This page outlines the eligibility criteria, amount of stamp duty relief, residential requirements for contracts to purchase entered into on or after 6 June 2024. If you entered into your contract to purchase between 15 June 2023 and 5 June 2024 please see the eligibility criteria, amount of stamp duty relief, residential requirements for contracts entered into between 15 June 2023 and 5 June 2024 page

Who is eligible for stamp duty relief?

You may be eligible for relief if you are:

- an Australian citizen or permanent resident. New Zealand citizens permanently residing in Australia who hold Special Category Visas may also apply. Only one applicant is required to meet this eligibility requirement.

- at least 18 years of age at the time of making application for stamp duty relief.

- a natural person.

Companies and trusts are not eligible for stamp duty relief, except in the case of a Special Disability Trust.

In addition, you or your spouse/domestic partner must not have:

- occupied an Australian residential property in which you had a relevant interest for 6 months or longer; or

- previously received stamp duty relief for eligible first home buyers (or equivalent) in any state or territory of Australia. If relief was received but later paid back together with any penalties incurred, you may be entitled to reapply for relief.

At least one applicant must reside in the home as their principal place of residence for a continuous period of at least six months commencing within:

- 12 months from the date of settlement, for contracts to purchase a new home.

- 12 months of the date the Certificate of Occupancy (the date you can lawfully live in the property) is issued or 36 months from the settlement date, whichever occurs first, for contracts to purchase vacant land.

The stamp duty relief is payable on the property regardless of the number of applicants.

No, there is no requirement to be in a relationship (married, registered relationship or de facto) or be domestic partners to apply for stamp duty relief for eligible first home buyers.

The relief extends to all first home buyers, regardless of their relationship to each other. For example, the applicants could be a married couple, mother and daughter, siblings or friends. However, all applicants and their spouse/domestic partner must meet the eligibility criteria. The relief also applies to sole purchasers.

If you have a spouse/domestic partner who will not be an owner of the property, you will need to include their details on the application form.

No, personal income or wealth is not part of the eligibility criteria.

Owner builders can apply for stamp duty relief if purchasing vacant land which they intend to build their principal place of residence on.

No, companies and trusts are not eligible to receive stamp duty relief.

It is possible however for a person with a legal disability, holding an equitable interest, to claim stamp duty relief, providing that the legal interest is held on trust by their guardian(s). In this situation, the equitable interest qualifies as a relevant interest and the legal interest does not (meaning that the eligibility of the trustee(s) is not a factor).

What type of property is eligible for stamp duty relief?

If you are a first home buyer you may be eligible for stamp duty relief if you are buying:

- a new home* (including a house, flat, unit, townhouse or apartment); or

- an off-the-plan apartment;

- a house and land package (contract to build - comprehensive building contract); or

- vacant land to build your new home on;

in South Australia and that home will be your principal place of residence.

* New home – a home that has not been previously occupied or sold as a place of residence, including a substantially renovated home.

The stamp duty relief for eligible first home buyers is not available on the purchase of an established home, including where the plan is to knock down and rebuild a new home. This includes where you subdivide the land, and your new home is built on one piece of the land.

The improvements on the land must be a fixed dwelling that is suitable as a residence, for example, a single dwelling, duplex, flat or townhouse.

You cannot receive stamp duty relief for a property used solely for investment purposes.

At least one applicant is required to occupy their property as their principal place of residence for a continuous period of least 6 months, commencing within 12 months after the completion of their transaction.

The substantially renovated home must be purchased from a developer, who has undertaken substantial renovations, not just purely cosmetic changes.

The developer must be registered for GST purposes for developing the property and claimed GST offsets on the renovations to the home and provide evidence of this.

When does stamp duty relief apply from?

Full stamp duty relief is available to eligible first home buyers who enter into a contract to purchase a new home, an off-the-plan apartment, vacant land or house and land (contract to build – comprehensive building contract) on or after 6 June 2024.

Entered into your contract to purchase between 15 June 2023 and 5 June 2024? View information on stamp duty relief relevant to you.

No, full stamp duty relief only applies to contracts entered into on or after 6 June 2024.

However if the value of the new home less than $700,000, you may be eligible for partial relief if the contract was entered into between 15 June 2023 and 5 June 2024.

If you entered into a contract to purchase a new home, an off-the-plan apartment, vacant land or house and land (contract to build – comprehensive building contract) before 15 June 2023, and subsequently have had to cancel that contract, you may still be eligible for stamp duty relief.

However, if the original contract and your new contract are for the purchase of the same new home or vacant land, RevenueSA may not accept the new contract and therefore the stamp duty relief for eligible first home buyers will not apply.

If this applies to you, please provide to RevenueSA a copy of the original contract and the new contract along with a brief explanation of why your contract was cancelled.

No, stamp duty relief only applies to contracts entered into on or after 15 June 2023.

If you entered into a contract to purchase a new home, an off-the-plan apartment, vacant land or house and land (contract to build – comprehensive building contract) before 6 June 2024 where the value was above $650,000, and subsequently have had to cancel that contract, you may still be eligible for stamp duty relief.

However, if the original contract and your new contract are for the purchase of the same new home or vacant land, RevenueSA may not accept the new contract and therefore the stamp duty relief for eligible first home buyers will not apply.

If this applies to you, please provide to RevenueSA a copy of the original contract and the new contract along with a brief explanation of why your contract was cancelled.

Am I eligible if I own, or have previously owned, residential property?

If you own, or previously owned, a residential property in Australia, which you resided in for a continuous period of 6 months or more you will not be eligible for stamp duty relief.

You may be eligible for stamp duty relief, where you:

- did not reside in the residential property that you own, or have previously owned; or

- own, or previously owned, vacant land.

Commercial, primary production or industrial land is not considered to be residential land and ownership will not exclude you from stamp duty relief.

Yes, if you own, or previously owned, vacant land you may still be eligible for stamp duty relief if you enter into a contract to purchase a new home, or vacant land with the intent of building your home, on or after 15 June 2023.

No. Stamp duty relief is only available if you entered into a contract to purchase the vacant land on or after 15 June 2023 (which may also incorporate a contract to build).

If you owned vacant land prior to 15 June 2023 and enter into a contract to build on or after the 15 June 2023 you will not be eligible for stamp duty relief.

If you own, or previously owned, residential property (in any Australian state or territory in which you resided for a continuous period of 6 months or more you will not be eligible for stamp duty relief.

If you did not reside in the residential property for a continuous period of 6 months or more, you may be eligible if you did not receive stamp duty relief for eligible first home buyers (or equivalent) in that state or territory.

A business premise is not considered a home for stamp duty purposes unless it could also be lawfully used for residential purposes.

You can, but may not be eligible for stamp duty relief if the other person occupied the property they had a previous relevant interest in as a place of residence for 6 continuous months or longer.

Yes, you may be eligible for stamp duty relief.

The rules regarding ownership only apply to residential property within Australia.

What if my spouse/domestic partner owns, or previously owned, residential property?

You may be eligible for stamp duty relief if your spouse/domestic partner owns, or previously owned, residential property and your spouse/domestic partner did not occupy that residential property as a place of residence for a continuous period of 6 months or longer.

If your spouse/domestic partner occupied the residential property as a place of residence for a continuous period of 6 months or more, you will not be eligible.

You must include your spouse/domestic partner on your application, even if they will not hold a relevant interest in the home.

If you are divorced or separated, any residential land your previous spouse/domestic partner owns, or previously owned, will not be considered as part of your application. You will be eligible for stamp duty relief provided you meet all eligibility criteria.

You will need to provide a copy of your divorce certificate or statutory declaration to confirm the separation.

Vacant land is not regarded as residential property for stamp duty relief purposes.

A person is the domestic partner of another if they live together in a close personal relationship.

A close personal relationship is defined to mean the relationship between two adult persons (whether or not related by family and irrespective of their gender) who live together as a couple on a genuine domestic basis, but does not include:

- the relationship between a legally married couple; or

- a relationship where one of the persons provides the other with domestic support or personal care (or both) for fee or reward, or on behalf of some other person or an organisation of whatever kind.

Note: Two persons may live together as a couple on a genuine domestic basis whether or not a sexual relationship exits or has ever existed, between them.

When will stamp duty relief apply to a new home?

Full stamp duty relief is available on the transfer of a new home or a substantially renovated home. This includes a contract to purchase a new home or an off-the-plan apartment.

The new home must not have been previously occupied or sold as a place of residence.

The contract to purchase must have been entered into on or after 6 June 2024.

Entered into your contract to purchase between 15 June 2023 and 5 June 2024? View information on stamp duty relief relevant to you.

No, full stamp duty relief only applies to contracts entered into on or after 6 June 2024.

However if the value of the new home less than $700,000, you may be eligible for partial relief if the contract was entered into between 15 June 2023 and 5 June 2024.

If you entered into a contract to purchase a new home, an off-the-plan apartment, vacant land or house and land (contract to build – comprehensive building contract) before 15 June 2023, and subsequently have had to cancel that contract, you may still be eligible for stamp duty relief.

However, if the original contract and your new contract are for the purchase of the same new home or vacant land, RevenueSA may not accept the new contract and therefore the stamp duty relief for eligible first home buyers will not apply.

If this applies to you, please provide to RevenueSA a copy of the original contract and the new contract along with a brief explanation of why your contract was cancelled.

No, stamp duty relief only applies to contracts entered into on or after 15 June 2023.

If you entered into a contract to purchase a new home, an off-the-plan apartment, vacant land or house and land (contract to build – comprehensive building contract) before 6 June 2024 where the value was above $650,000, and subsequently have had to cancel that contract, you may still be eligible for stamp duty relief.

However, if the original contract and your new contract are for the purchase of the same new home or vacant land, RevenueSA may not accept the new contract and therefore the stamp duty relief for eligible first home buyers will not apply.

If this applies to you, please provide to RevenueSA a copy of the original contract and the new contract along with a brief explanation of why your contract was cancelled.

When will stamp duty relief apply to vacant land?

Full stamp duty relief is available on the transfer of vacant land, where you intend to build your principal place of residence. Vacant land includes where you have entered into a contract for a house and land package (usually a comprehensive building contract).

The contract to purchase must have been entered into on or after 6 June 2024.

Entered into your contract to purchase between 15 June 2023 and 5 June 2024? View information on stamp duty relief relevant to you.

Stamp duty relief may have been available on the transfer of vacant land. No further relief is available.

If you are eligible for the stamp duty relief for eligible first home buyers and relief was not applied on the transfer of your land, you can apply for a refund by completing the Application for refund of stamp duty (online) and provide any required supporting documentation including the completed Application for Stamp Duty Relief for Eligible First Home Buyers (PDF 406KB).

When do I need to move into the home?

In the case of a new home or an off-the-plan apartment, you must reside in the home as your principal place of residence for a continuous period of at least 6 months, commencing within 12 months of date of settlement.

In the case of vacant land, you must move into the home as your principal place of residence within:

- 12 months of the date the Certificate of Occupancy is issued (the date you can lawfully live in the property); or

- 36 months of the settlement date;

whichever occurs first.

If you buy the home with someone else, or multiple people, only one of you is required to satisfy the residency requirements.

It is your responsibility to meet the residency requirements. You may be required to verify this later by providing documentation supporting your period of occupancy (for example: electricity and gas accounts, bank statements, landline and/or mobile phone accounts and household contents insurance policies).

If you will not meet the residency requirements, you must contact RevenueSA in writing within 14 days of the date on which it first becomes apparent you will not be able to comply with the residency requirements and pay the stamp duty applicable.

The most important characteristic of a person’s principal place of residence is that the person is living in that residence on an ongoing or permanent basis as the person’s settled or usual place of abode. Mere residence is insufficient, even where that residence is for the requisite continuous 6 month period. Where the occupation is transient, temporary or of a passing nature, or where occupation is for some other purpose, such as preparing the home for sale or rental, this will not qualify as occupation as a principal place of residence.

Whether an applicant has occupied a property as their principal place of residence is a question of fact having regard to all of the circumstances. The intention of the applicant is relevant but is not determinative of the issue.

In general terms, an applicant’s settled or usual place of abode is the place where the person ordinarily cooks, eats, sleeps and conducts most other activities of daily living and has the characteristics of permanency.

At least one applicant must live in the home as their principal place of residence for at least 6 continuous months commencing within:

- 12 months after the date of settlement for new homes and off-the-plan apartments; or

- 12 months after the date the Certificate of Occupancy is issued or 36 months from settlement (whichever occurs first) for vacant land (also includes a house and land package).

It is the responsibility of the applicant to meet the residency requirement. Applicants may be required to verify this later by providing documentation supporting their period of occupancy.

Should you not meet the residency requirement, you must contact RevenueSA in writing within 14 days after becoming aware that you will not comply.

You must occupy the home for a continuous period of at least 6 months commencing within:

- 12 months after the date the Certificate of Occupancy is issued; or

- 36 months from settlement:

whichever occurs first.

You must occupy the home for a continuous period of at least 6 months commencing within:

- 12 months after the home becomes ready for occupation; or

- 36 months from settlement:

whichever occurs first.

No. At least one applicant must occupy the relevant home as their principal place of residence:

New home or off-the-plan apartment:

for a continuous period of at least 6 months commencing within:

- 12 months after the date of settlement.

Vacant land or house and land package:

for a continuous period of at least 6 months commencing within:

- 12 months after the date the Certificate of Occupancy is issued; or

- 36 months from settlement;

whichever occurs first

Providing you occupy the home as your principal place of residence:

New home or off-the-plan apartment:

for a continuous period of at least 6 months commencing within:

- 12 months after the date of settlement.

Vacant land or house and land package:

for a continuous period of at least 6 months commencing within:

- 12 months after the date the Certificate of Occupancy is issued; or

- 36 months from settlement;

whichever occurs first

you are still eligible for stamp duty relief.

It is also acceptable for you to rent out a room (or other portion of the home) while you complete your 6 months' occupation.

If you believe that you may not have met the residency requirements, you must advise RevenueSA in writing within 14 days of your circumstances changing. Upon receipt of such written advice, RevenueSA will commence an investigation to determine your eligibility to retain any stamp duty relief received.

The Commissioner may vary an applicant's residency requirement if satisfied there are good reasons for doing so.

If an applicant fails to notify RevenueSA that the residency requirements have not been met, penalties may be imposed. The amount of any penalty which may apply is dependent on the circumstances of each case and is in addition to having to pay the stamp duty applicable.

The residence requirement does not apply to members of the Australian Defence Force.

You must be a current member of the Australian Army, Air Force or Navy and be enrolled to vote in South Australian elections. If you are buying your home with another person who is not a member of the Australian Defence Force, they must be enrolled to vote in South Australian elections.

The exemption does not apply to Australian Army, Air Force or Navy reservists or to Australian Public Service staff.

How much stamp duty relief is available?

If you are a first home buyer and eligible for the stamp duty first home buyer relief, the relief may reduce your stamp duty to zero if your contract was entered into on or after 6 June 2024.

Entered into your contract to purchase between 15 June 2023 and 5 June 2024? View information on stamp duty relief relevant to you.

Stamp duty relief may still apply providing all eligibility criteria is met.

No, there is no minimum amount that must be paid, you will only receive stamp duty relief equal to the stamp duty applicable to the dutiable value of the transaction.

No. Stamp duty relief is only available if you entered into a contract to purchase the vacant land on or after 15 June 2023 (which may also incorporate a contract to build).

If you owned vacant land prior to 15 June 2023 and enter into a contract to build on or after the 15 June 2023 you will not be eligible for stamp duty relief.

Will the foreign ownership surcharge be applied if one or more of the owners is not an Australian citizen or permanent resident?

If all eligibility criteria are met, the foreign ownership surcharge will not apply on:

- new homes or off-the-plan apartments with a dutiable value of $650,000 or less

- vacant land with a dutiable value of $400,000 or less (includes a house and land package, where the land value is $400,000 or less)

The foreign ownership surcharge only applies where stamp duty is payable, therefore it will apply on:

- new homes or off-the-plan apartments with a dutiable value above $650,000

- vacant land with a dutiable value above $400,000(includes a house and land package, where the land value is above $400,000)

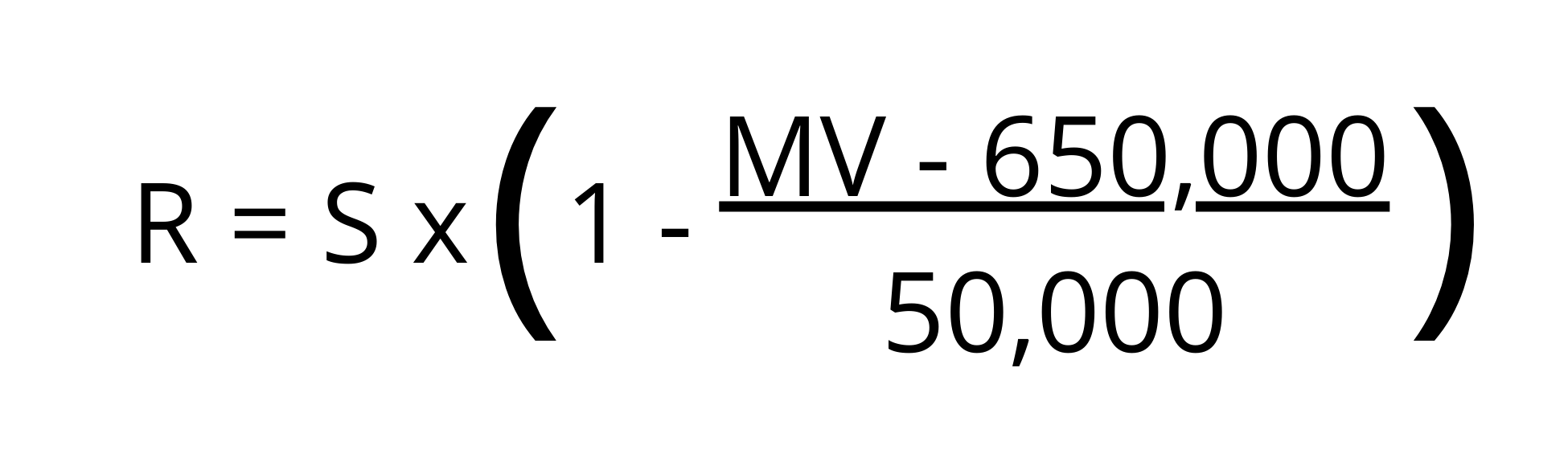

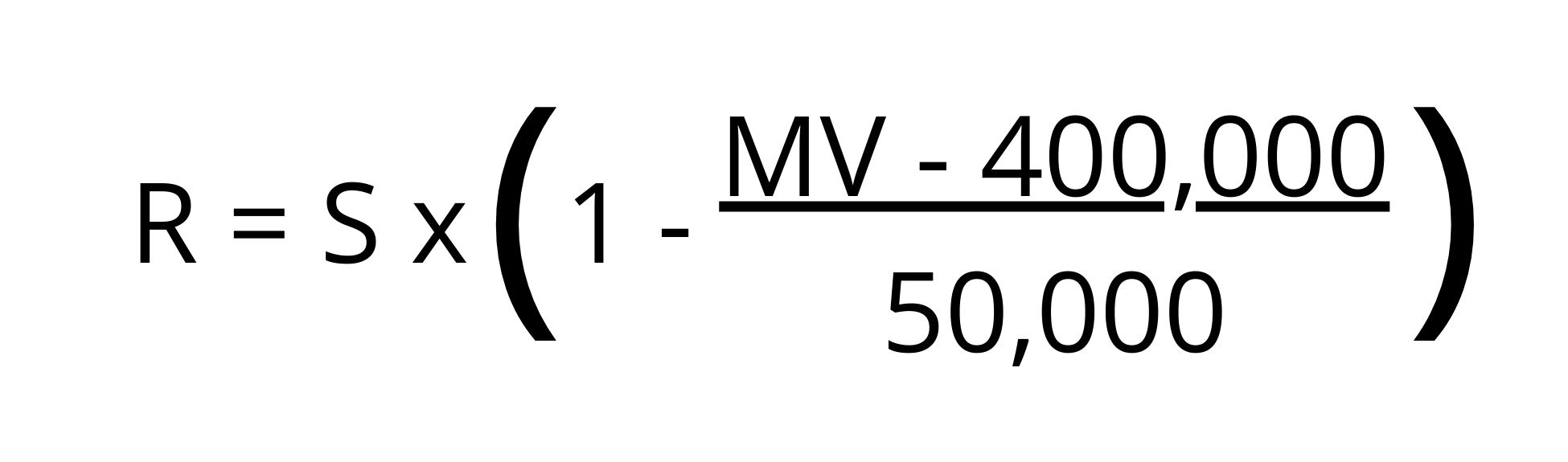

Where the dutiable value of a new home, substantially renovated home or off-the-plan apartment is below $700,000 or if vacant land is below $450,000 – the applicant will receive partial stamp duty relief calculated on the total of the stamp duty and foreign ownership surcharge. In these cases, the foreign ownership surcharge is applied at 7% on the interest the foreign owner has in the land. The stamp duty relief will be calculated on the total of the stamp duty and foreign ownership surcharge using the following formulas:

Where :

- R is the amount of reduction in stamp duty

- S is the total of stamp duty and foreign ownership surcharge that would apply if relief was not provided

- MV is the market value of the new home (including the land on which the home is situated)

Where :

- R is the amount of reduction in stamp duty

- S is the total of stamp duty and foreign ownership surcharge that would apply if relief was not provided

- MV is the market value of the vacant land

How do I apply?

All intended owners must be included on the application and meet all eligibility criteria.

You need to complete an Application for Stamp Duty Relief for Eligible First Home Buyers (PDF 406KB) and provide it to the representative managing the settlement of your property (for example, conveyancer or solicitor) along with any required supporting documentation.

All transactions for which stamp duty relief is sought must be lodged for an assessment by the Commissioner of State Taxation. The transaction cannot be self-determined.

If you are not using a representative, you can lodge directly to RevenueSA by email to sdrequisitions@sa.gov.au. You must provide

- Application for Stamp Duty Relief for Eligible First Home Buyers (PDF 406KB) and supporting documentation

- Application for Stamp Duty Assessment (PDF 220KB)

- Transfer document (T1)

- Contract for sale.

If you are eligible for the stamp duty relief for eligible first home buyers but have already purchased a new home or vacant land and settlement has been finalised, you can apply for a refund by completing the Application for refund of stamp duty (online) and providing any required supporting documentation including the completed Application for Stamp Duty Relief for Eligible First Home Buyers (PDF 406KB).

Yes. The eligibility criteria applies to both the applicant and the applicant's spouse/domestic partner.

If your spouse/domestic partner will hold a relevant interest in the home, they must complete the ‘Section 2 Applicant (Purchaser) Details’ section of the application.

If your spouse/domestic partner will not hold a relevant interest in the home, they must complete the ‘Section 3 Spouse/Domestic Partner Details’ section of the application.

What supporting documentation must I provide?

You will need to provide:

Proof of Identity

Each applicant and their spouse/domestic partner must provide at least one document from the below list.

- Australian Birth Certificate

- Australian Certificate of Registration by Descent

- Australian Change of Name Certificate

- Australian Citizenship Certificate

- Australian Driver’s Licence

- Australian ImmiCard

- Australian Marriage Certificate

- Australian Medicare Card

- Australian Passport or Travel Document

- Australian Visa

Please ensure all copies provided are legible.

Note: Evidence of change of name is required if the name on any of the documents presented is different to the name of the applicant, for example, marriage certificate, change of name certificate.

Proof of Citizenship or permanent residency

Primary identity document and evidence of citizenship or permanent residency (provide one document):

If an Australian citizen:

- Australian Birth Certificate issued by Births, Deaths & Marriages (Office of Consumer & Business Affairs).

- current Australian Passport.

- Citizenship Certificate or Australian Certificate of Registration by Descent.

If a New Zealand citizen:

- current New Zealand passport.

Note: New Zealand citizens must be living in Australia at the time of application.

If a citizen of another country:

- current passport; and

- evidence of permanent residency or permanent residence visa.

Note: At least one applicant must be an Australian citizen or permanent resident. All applicants must be living in Australia.

Note: Australian Citizen Certificate or Permanent Residency Visa must have been issued on or before the lodgement of the application for stamp duty relief for eligible first home buyers.

Note: Evidence of change of name is required if the name on any of the documents presented is different to the name of the applicant, for example, marriage certificate, change of name certificate.

Transaction Type

Contract to purchase a new home or off-the-plan apartment

- a copy of the Contract for Sale, dated and signed by the vendor and purchaser; and

- a copy of the transfer of land (T1)

Plus, one of the following documents:

- a written statement from the vendor confirming the home has not previously been sold or occupied as a place of residence (if you are purchasing a new home)

- a copy of the Certificate of Occupancy (if purchasing an off-the-plan apartment)

- evidence that the developer is registered for GST purposes for developing the property and claimed GST offsets on the renovations to the home (if purchasing a substantially renovated home)

Contract to build (House and land package, comprehensive building contract)

- a copy of the Contract to build dated and signed by all parties

- a copy of the Contract for Sale, dated and signed by the vendor and purchaser

- a copy of the transfer of land

Contract to purchase vacant land

- a copy of the Contract for Sale, dated and signed by the vendor and purchaser

- a copy of the transfer of land

Additional supporting evidence is required if any of the following apply to you:

If you are married

A copy of your marriage certificate.

If you are divorced

A copy of your divorce certificate.

If you are widowed

Copy of the death certificate of your spouse/domestic partner.

If you are separated

A Statutory Declaration with the following information:

- the name of your former spouse/domestic partner

- former spouse/domestic partner’s date of birth

- the date you were married or commenced cohabiting in a domestic partnership

- the date you separated

- your former spouse/domestic partner’s current address (if known); and

- a statement to the effect that you do not live together and have no intention of resuming cohabitation.

If you have a representative managing the settlement of your property (for example, conveyancer or solicitor) please provide your supporting documentation to them with your application form.

If you are lodging directly to RevenueSA, please include your supporting documentation when you lodge your transfer document for assessment by emailing sdrequisitions@sa.gov.au.

If I purchase a home and receive stamp duty relief, but later resell the home, do I have to pay stamp duty?

New home or off-the-plan apartment

Providing that at least one of the applicants occupied the home or apartment as their principal place of residence for a continuous period of at least 6 months, commencing within 12 months after the date of settlement, you will not be required to pay the stamp duty that your relief applied to.

Vacant land or house and land package

Providing that at least one of the applicants occupied the home as their principal place of residence for a continuous period of at least 6 months, commencing within:

- 12 months after the date the Certificate of Occupancy is issued; or

- 36 months from settlement;

whichever occurs first, you will not be required to pay the stamp duty that your relief applied to.

If I received stamp duty relief, will I be expected to pay stamp duty if I don’t meet the eligibility criteria?

Yes. If you receive stamp duty relief, but you or another applicant are not entitled to relief, or do not comply with the residency requirement, you must pay the stamp duty applicable. Penalties may be imposed. The amount of any penalty which may apply is dependent on the circumstances of each case and is in addition to also having to pay the stamp duty applicable.

See the Interest and Penalty Tax page for more information.

Penalty

RevenueSA, as part of its role in administering the Stamp Duties Act 1923, conducts ongoing investigations to ensure that applicants comply with the conditions of the stamp duty relief.

If you receive stamp duty relief that you are not entitled to, or you do not comply with the residency requirement, penalty may be imposed. The amount of any penalty which may apply is dependent on the circumstances of each case and is in addition to having to pay the stamp duty.

See the Interest and Penalty Tax page for more information.

Providing incorrect or misleading information in this application

Dishonestly providing incorrect or misleading information to RevenueSA is a criminal offence. If it is determined that you have provided incorrect or misleading information to obtain, or attempt to obtain stamp duty relief, legal action may be commenced.

All applications undergo a rigorous review where applicants are checked for former and/or current residential property ownership in South Australia and interstate. Other checks into spouse/domestic partner status, council records, title details and finance particulars are also undertaken on a routine basis.

Examples

Example 1

Sunny & David enter into a contract on 10 August 2025 to purchase a new house with a purchase price of $870,000.

Sunny and David may be eligible for full stamp duty relief of $41,680 (being the stamp duty applicable on $870,000) on the land transfer, provided that all other eligibility criteria are satisfied. Sunny and David will not be required to pay stamp duty on the transfer.

Example 2

Mark enters into a contract on 22 August 2025 to purchase a house and land package with a total purchase price of $485,000. The contract specifies:

- $250,000 for the land; and

- $235,000 for construction of the house

In September 2025, the title for the land transfers to Mark before building commences. As the land is vacant at the time of transfer, the dutiable value of the transfer is $250,000.

Mark may be eligible for full stamp duty relief of $8,955 (being the stamp duty applicable on $250,000) on the land transfer, provided that all other eligibility criteria are satisfied. Mark will not be required to pay stamp duty on the transfer.

Example 3

Paul enters into a contract on 15 September 2024 to purchase vacant land. The purchase price is $395,000. Paul intends to build his principal place of residence on the land.

Paul may be eligible for full stamp duty relief of $16,080 (being the stamp duty applicable on $395,000) on the land transfer, provided that all other eligibility criteria are satisfied. Paul will not be required to pay stamp duty on the transfer.

Example 4

Brooke enters into a contract to purchase a new home on 10 June 2023. The home has not been previously occupied or sold as a place of residence. The purchase price is $575,000.

As the contract was entered into before 15 June 2023, Brooke is not eligible for stamp duty relief and she will be required to pay stamp duty of $25,455 on the transfer.

Example 5

Peter and Mary enter into a contract to purchase a new home on 10 June 2024. The home has not been previously occupied or sold as a place of residence. The purchase price is $640,000 and they will each have a 50% interest in the home.

Peter is an Australian citizen, while Mary is not.

As the dutiable value of the property does not exceed $650,000, Peter and Mary may be eligible for full stamp duty relief of $29,030 (being the stamp duty applicable on $640,000) on the land transfer, provided that all other eligibility criteria are satisfied.

As the dutiable value of the property does not exceed $650,000 and the contract was entered into before the Statute Amendment (Budget Measures) Bill 2024 has been passed, Mary (even though Mary is not an Australian citizen) will not liable for the foreign ownership surcharge on her interest in the land as no stamp duty applies.

Example 6

Zack enters into a contract to purchase a new home on 28 August 2024. The home has not been previously occupied or sold as a place of residence. The purchase price is $870,000.

Zack does not move into the new home until December 2025.

In this case Zack has not meet the residential requirements for a new home, in that he must reside in the home as his principal place of residence for a continuous period of at least 6 months commencing within 12 months after the date of settlement.

If Zack had applied and received stamp duty relief, he would be required to pay stamp duty of $41,680, that would have applied at settlement. Interest and penalty tax may also apply.